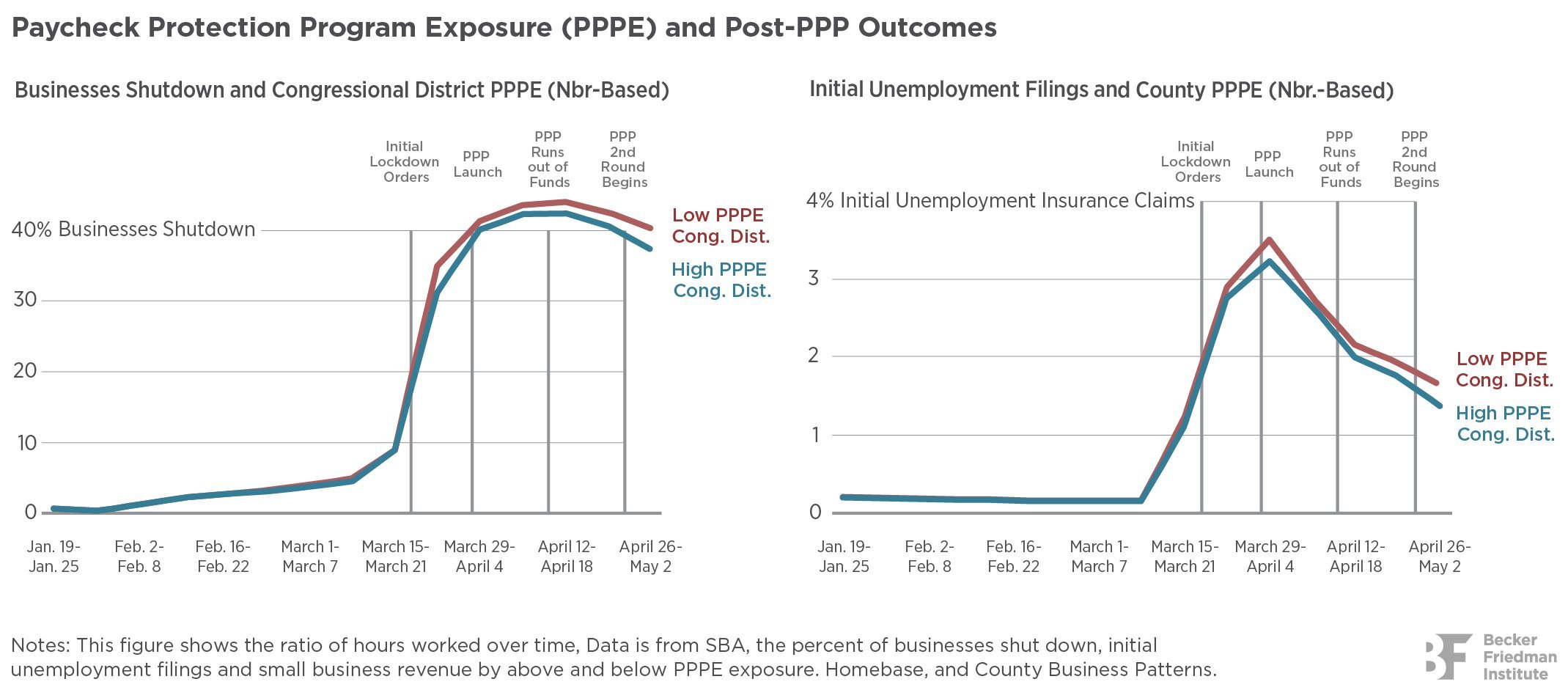

Key Economic Findings from UChicago Research

Summary analysis of the latest research from UChicago scholars, complementing the BFI Working Paper series that draws from more than 200 economists on campus.

Filter By

-

Children from low-income families have lower math test scores, on average, than their higher-income peers. These disparities are of concern in their own right and because early childhood math test scores tend to predict later outcomes. Evidence suggests that income-based achievement gaps are in part driven by unequal engagement from parents, with higher-income parents spending more time on math activities than lower-income parents. This study aims to uncover what drives these persistent gaps in achievement and parental engagement and, in turn, what policies and programs will effectively improve learning outcomes among low-income students.

The authors conducted a randomized controlled trial with 758 low-income preschoolers and their parents, who they separated into a control group and four treatment groups. The first treatment group received a set of math materials, the second received the same materials along with weekly text messages intended to overcome any tendency among parents to procrastinate doing math with their kids (referred to as “present bias”), and the third received the materials and weekly text messages promoting a growth mindset. Finally, the fourth treatment group received a digital tablet with math apps for children. The authors tested children’s math skills three times — before the intervention, upon the conclusion of the intervention, and six months afterwards — and surveyed parents regarding the amount of time that they spent doing math with their kids. They found the following:

- Relative to the control group, both the math app treatment and the material plus procrastination treatment increased children’s math skills six months after the intervention ended, while the other treatments did not increase children’s math skills.

- The two treatments that improved math skills also increased the amount of time that parents reported having spent engaging in math activities with their children, while the two treatments that did not increase math skills also did not increase the amount of time that parents reported having spent on math. This suggests that increased parent engagement is a mechanism that leads to improved math skills.

- A considerable share of parents (17%) in the materials-only group reported losing the materials, and only 37% finished half of the activities included in the materials. This limited use suggests that the provision of materials alone is insufficient to help low-income families overcome learning gaps.

- The survey data show that most parents already exhibit growth mindsets, thereby reducing the benefits of interventions that aim to cultivate growth mindsets in parents.

The upshot is that simply telling parents that they should engage in learning with their children, even if the materials for engagement are also provided, is unlikely to change their behavior. This is especially the case when parents are constrained by psychological stress or financial scarcity. The results also indicate that a potential barrier preventing parents from using math materials when they are available is present bias, or the tendency to procrastinate when a reward is delayed. Finally, the surprising effectiveness of the math app treatment on both parent engagement and test scores suggests a new, lost-cost avenue for improving children’s math skills at home.1

1 See also “Nudging or Nagging? Conflicting Effects of Behavioral Tools,” by Ariel Kalil, et al., for a Finding and links to the paper.

-

Labor market policies, which include programs such as vocational training, job search aid, and wage subsidies, are of increasing importance for ensuring a productive workforce amid ongoing structural changes in the labor market. Despite this, there is limited evidence regarding their effectiveness. Workers who opt into training programs likely differ systematically from those who do not, casting doubt on the results of studies that simply compare the outcomes of workers who do and do not complete training. This study overcomes this limitation by using data on jobseekers who are quasi-randomly matched with caseworkers to assess the impacts of a particular labor market policy in Denmark — classroom training.

The authors use administrative data from Denmark covering jobseekers who lost their jobs between 2012 and 2018. Importantly, for unemployed jobseekers to receive UI benefits from the Danish government, they must meet with a caseworker at a job center to receive assistance with their job search and assignment to a training program. Jobseekers are assigned caseworkers essentially randomly (based on their day of birth), and caseworkers differ in their tendencies to assign jobseekers to different types of training programs, with some caseworkers more likely to assign jobseekers to classroom training programs and others more likely to assign jobseekers to programs that provide training on the job. The authors exploit this in their research design and compare the employment outcomes of jobseekers from the same job center and year who, due to their day of birth, receive different counseling. They find the following:

- Jobseekers who are assigned to classroom training tend to work more as a result. These employment gains grow steadily over time, stabilizing at about 25 hours more per month two years after their initial job loss, equivalent to a 25% increase relative to before their job loss.

- By contrast, on-the-job-training programs, such as employment programs with wage subsidies, do not lead to employment gains.

- These results diverge from earlier studies that rely on observable characteristics of jobseekers and often conclude that classroom training has deleterious effects on employment. By contrast, this work accounts for selection based on unobserved characteristics when evaluating labor market policies; for example, jobseekers who face worse employment prospects are more likely to opt into training.

In the next part of the paper, the authors aim to uncover the mechanisms driving the effects revealed in their analysis. They find the following:

- The benefits of workforce training are driven primarily by the positive effects accrued by participants who complete the programs, rather than by jobseekers who simply exit unemployment upon commencing training. This suggests that classroom training increases employment by providing job seekers with skills that are valued in the labor market.

- Assignment to classroom training especially increases employment outside jobseekers’ original occupations, providing further support for the conclusion that workforce training helps workers find jobs through the provision of new skills.

- The employment effects of classroom training are driven by participants’ more successful job applications rather than by their intensified job searches, again underscoring the role of skill acquisition.

The authors conclude by exploring how these effects vary across different types of workers in order to offer insights relevant for policy:

- Jobseekers who are employed in occupations that are more exposed to offshoring have higher employment gains from classroom training. By quarter seven after their initial job loss, high-risk jobseekers gain 55 hours of employment per month from assignment to classroom training. This gain corresponds to 50% of their pre-job-loss level of employment.

- In contrast, jobseekers at low risk of offshoring derive much lower employment gains from assignment to classroom training. By quarter seven after their initial job loss, the gains for low-risk job seekers are not statistically significantly different from zero.

- Taken together, these results suggest that a cost-effective way to close the employment gap is to redistribute classroom training from low-risk to high-risk jobseekers. Note that this counterfactual scenario corresponds to assigning 25% of all job seekers to classroom training, compared to today’s 39%. Hence, this policy would lower total spending on classroom training programs while bolstering their effect on employment.

This paper provides novel evidence for the effectiveness of classroom training for helping displaced workers regain employment. From a methodological standpoint, this study illustrates the potential pitfalls in assigning causality in studies lacking at least quasi-randomness. For policymakers, this research offers a tool for closing the employment gap among job seekers affected by offshoring.

-

One persistent question in economics over the last 150 years is whether rising production concentration is somehow inevitable in modern industrial development. Since the 19th century and including Marx, continuing through Alfred Marshall near the dawn of the 20th, and onward to the present, many have wondered whether increasing concentration is mere coincidence or, perhaps, an economic law. Lenin certainly believed that concentration was inexorable, confidently stating in 1916: “[T]he enormous growth of industry and the remarkably rapid concentration of production … are one of the most characteristic features of capitalism.”

What happened in the century following Lenin’s assertion? This research examines this question by studying the evolution of production concentration in the US economy from 1918 to 2018. The authors develop a rich database by digitizing data on US corporations from the historical publications of the Statistics of Income (SOI) and the associated Corporation Source Book from the Internal Revenue Service (IRS). Since 1918, the SOI has been reporting annual statistics of the population of corporations by size bins, including the number of businesses and their financial information (e.g., assets, sales, net income,). Please see the working paper for more details on methodology. The authors use these size bins to estimate top businesses’ shares in the aggregate, in main sectors, and in subsectors, to find the following:

- Since the early 1930s, the asset shares of the top 1% and top 0.1% corporations have increased by 27 percentage points (from 70% to 97%) and 40 percentage points (from 47% to 88%), respectively.

- At the industry level, the authors note a general rise in corporate concentration among the main sectors and the subsectors, but the timing differs across industries. For manufacturing and mining, rising concentration was stronger in earlier decades (before the 1970s); for services, retail, and wholesale, rising concentration was stronger in later decades (after the 1970s).

- These results hold when the authors examine the relative concentration within the largest businesses (e.g., the top 1% relative to the top 10%), when they include noncorporations (partnerships and sole proprietorships) in years with available data, as well as when they review a fixed number of businesses (e.g., top 500 or 5,000).

The authors acknowledge that it is challenging to determine the precise cause of this persistent increase in corporate concentration, but they offer insights into the leading hypotheses, including the following:

Economies of scale

In line with previous research that has shown how industrial technologies have spurred concentration trends among US corporations1, they find that:

- The timing and the degree of rising concentration in an industry align closely with rising technological intensity, for example, the top 1% share in an industry comoves strongly with the investment intensity of R&D and IT. Also, patent data reveal that influential technologies are associated with more production concentration (whereas the total number of patents, per se, does not play a role).

- The degree of concentration is positively correlated with a measure of the intensity of fixed operating costs. In other words, to the degree that higher fixed costs favor production at scale, large firms have an advantage.

- Over the medium term, industries that experience higher increases in concentration also experience higher growth in real gross output, and their output shares in the economy expand.

Trade and globalization

International trade is not sufficient to explain industrial concentration trends over the last 100 years:

- For the United States, trade did not expand in the first half of the 20th century when manufacturing concentration was on the rise.

- Also, globalization only accelerated around the 1970s, when the rise in services concentration took hold; however, the volume of international trade in services is relatively small.

Regulation

On the question of whether, and to what degree, regulation has influenced corporate concentration, the authors find that:

- The data do not reveal a significant relationship between corporate concentration and standard aggregate antitrust enforcement measures, such as the number of antitrust cases filed by the Department of Justice (DOJ) or the budget of the DOJ’s antitrust division.

- That said, antitrust regulation could

have a more pronounced impact on a particular market. - In sum, the authors do not find that regulations have shifted in favor of large firms over the past century; moreover, they find no evidence that regulations particularly favored manufacturing over services in earlier decades, and then switched focus post-1970.

Bottom line: Long-run trends of US corporate concentration are likely explained by economies of scale. As to whether such concentration is “good” or “bad,” the welfare implications can be nuanced. For example, even if large firms emerge from economies of scale over time (that is, from seemingly “good” or at least “neutral” causes), their size may ultimately allow firms to wield power that unduly benefits them at the cost of, say, social wellbeing (an arguably “bad” outcome).

On the intriguing question of whether corporate concentration will persist into the future, the authors suggest that—historical evidence notwithstanding—the answer is not obvious.

At the turn of the 20th century, the inevitability of technological changes leading to increasingly larger enterprises and higher production concentration was a central doctrine of communism, with Lenin asserting that economies of scale due to “modern technology” would be so strong that the Soviet Union could be run by one giant firm to enhance efficiency. Though extreme, this view inspired the work of Ronald Coase on the boundaries of the firm, and influenced the direction of a number of prominent intellectual traditions. Some maintain that large enterprises will become all powerful and change the way society is organized, whereas others caution that large organizations face certain limitations. Which direction will we go? More analyses about the nature of the firm and the foundations for the organization of production may provide knowledge that can guide our outlook.

For more on the history of thought about the organization of production and the organization of society, please see Yueran Ma’s video presentation “Communism and the Chicago School.”

1 See “The Industrial Revolution in Services,” forthcoming from Journal of Political Economy, by UChicago economists Chang-Tai Hsieh and Esteban Rossi-Hansberg, for additional insights into methodology and findings related to US industrial concentration over the last 50 years; available as a BFI Working Paper, Research Brief, and Economic Finding.

-

Capital markets for large multinational firms can be characterized as external (when capital is supplied by a bank or bond markets, for example) or internal (wherein a firm issues capital to business units in the form of, say, redistributed profits). Of the two, we know less about the inner workings of internal capital, despite their prominence in global capital movements. In recent years, for example, internal capital flows between multinational parent firms and their international affiliates accounted for over 50 percent of total capital inflows in the median country. Internal capital flows are also large relative to aggregate output, amounting to 3.6 percent of GDP in the median country.

We also understand little about how internal capital markets impact the real economy. Do internal capital markets transmit shocks across countries? Which mechanisms and frictions play a role, like managerial biases, access to external credit markets, different currencies, and geographic distance? Do internal capital markets transmit financial and non-financial shocks differently? How large and persistent are the real effects of internal capital market shocks?

To address these questions, the authors study a lending cut by Commerzbank, Germany’s second-largest bank in 2008, whose corporate lending was concentrated in Germany. During the 2008-09 Financial Crisis, Commerzbank experienced significant losses on its financial investments that, while independent of Commerzbank’s corporate lending division, ultimately impacted corporate borrowers because the losses forced Commerzbank to reduce its loan supply. This exogenous shock to the credit supply impacted those multinationals located in Germany with a higher pre-crisis dependence on Commerzbank, but did not directly affect the credit supply of international affiliates of these multinationals.

The authors examine whether and how this lending cut affected international affiliates of impacted German parent companies. In doing so, the authors compare affiliates located in the same country at the same time, so that differences in demand or other country-specific shocks do not affect the estimates. The authors investigate a number of ways that a credit shock to parents could transmit through internal capital markets and affect international affiliates, to find the following:

- Sales of affiliates with greater parent Commerzbank dependence dropped sharply once Commerzbank reduced lending in 2008 and took until 2011 to fully recover.

- Affiliates with greater parent Commerzbank dependence would have evolved in parallel to other affiliates had Commerzbank’s lending cut in Germany not happened.

- Affiliates with previous internal loans strongly increased lending to their parent after the lending cut, but other affiliates did not. Also, the reduction in affiliate sales was large and significant for affiliates that had previous internal loans and increased internal lending, but insignificant for other affiliates.

- Affiliates with greater internal lending suffered large and significant sales declines, while the effects on other affiliates were relatively small and insignificant.

- Frictions due to currency, geography, and capital controls were not important, but developed external credit markets helped affiliates to partially attenuate these effects.

- Location matters: Weak international affiliates were hit more strongly, which leads the authors to characterize managers of multinationals as relatively “Darwinist” with respect to international affiliates. In contrast, affiliates within Germany were not significantly harmed, even if they were weak, implying that managers have “Socialist” preferences toward home country affiliates.

- Regarding non-financial shocks, the authors examine how internal capital markets adjusted when parents were hit by a large-scale flood in 2013. They show that flooded parents were not financially constrained, suggesting that internal capital markets transmit financial shocks (like Commerzbank’s lending cut) more strongly than non-financial shocks.

- Finally, the authors analyze the transmission of Commerzbank’s lending cut through German multinationals in various countries, to reveal how a shock to an individual firm in one country can have first-order effects on the distribution of firm growth in many other countries, solely because of transmission through the internal networks of multinationals.

Bottom line: This work offers new and key insights into the role internal credit markets, including that shocks can transmit across affiliates, that internal capital flows across countries depend on different frictions than flows within domestic business groups, that financial shocks are transmitted strongly within internal capital markets while non-financial shocks have a weaker impact, and that internal capital flows can also cause financial constraints and thereby harm growth.

-

Mentorship is a common tool for increasing entrepreneurs’ likelihood of success as well as for closing gender gaps, particularly in developing countries where the share of owner-entrepreneurs is greater and gender gaps are more pronounced. This paper studies the role of gender matching in entrepreneurship, asking whether mentorship is more effective at improving female entrepreneurs’ odds of success when mentors are female as well.

Examples of Virtual Entrepreneur – Mentor Meetings

The authors conducted a randomized controlled trial in which they divided 930 Ugandan entrepreneurs into a treatment group and a control group. Next, members of the treatment group were also randomly assigned a mentor from whom they received up to six months of virtual business support. Two years later, the authors collected data on sales and profits at the entrepreneurs’ businesses, revealing the following:

- Female entrepreneurs benefited more from female mentorship than they did from male mentorship. Female entrepreneurs mentored by females saw their firm sales increase by 34% and profits by 29%, on average, compared to the control group. By contrast, female entrepreneurs guided by male mentors did not significantly improve their performance.

- Mentor gender did not matter for male entrepreneurs – there was no significant difference in the outcomes of those matched with a male mentor versus a female mentor.

What drives these effects? The authors conducted follow up analysis using written meeting summaries, data on customer relations, and information about entrepreneurs’ levels of aspiration. They found the following:

- Female mentors used significantly more relational language when describing their interactions with female entrepreneurs, suggesting that female mentors may have formed closer bonds with female entrepreneurs.

- Female entrepreneurs who were matched with female mentors seemed to significantly improve their relationships with customers, based on measures including closeness of engagement, follow-up communication incidence and transaction volume. These improvements in customer relations appear to largely explain the strong positive effects of female mentorship on women.

- Female entrepreneurs who reported higher aspiration levels before receiving mentorship tended to benefit significantly more from female mentors, suggesting that aspirational female entrepreneurs may be better targets for training programs aimed at driving economic growth when such programs are delivered by females.

This paper makes the case for same-gender mentorship as a tool for helping to overcome the pervasive barriers to business success faced by female entrepreneurs in developing economies. More broadly, the approach holds promise across the many contexts in which women’s advancement is stymied by “glass ceilings,” though future research is needed to determine where it will be most effective.

-

Technological progress is key to economic growth; likewise, economists have long focused on how many resources a society dedicates to research and development (R&D), whether in aggregate R&D spending or in the share of inventors in the workforce. However, this new research argues that focusing on the quantities of R&D investment misses an important point: It is not only the level of innovation inputs that matters for growth, but also the allocation of those investments.

The authors’ investigation has its grounding in a 1962 insight from the economist Kenneth Arrow, who intuited that monopolists have incentives to defend their market positions rather than produce radical technological breakthroughs. If true, this means that while the number of inventors and total R&D spending in an economy is important, the efficacy of that spending is mediated by where those inventors are employed.

Figure 1 illustrates the authors’ provocative hypothesis. Panel A shows total factor productivity (TFP)2 in the United States since 2000 (left axis) and a per capita measure of inventor labor (right axis). While there is a visible acceleration between 2000-2005, after 2005 there is a marked slow-down in TFP growth, even as the share of inventors grew by over 70%. In other words, innovation inputs are rising as technical progress slows. Equally striking is the shifting allocation of inventors across different-sized firms. Not only did the US economy allocate a bigger share of its employment into innovation, but its composition has also shifted toward the largest players in the economy.

Panel B shows that the share of inventors employed by large, incumbent firms rose from 48 percent in 2000 to about 57 percent in 2016 (in a 2022 paper, the authors show a complementary fall in the share of inventors employed by young firms3). Finally, Panel C shows that inventors at incumbents produce lower quality innovations, with fewer citations, fewer citations per application, fewer independent claims, and more self-citations (a proxy for the incremental nature of an innovation).

These figures raise an important question that motivates this research: How are inventors allocated in the US economy, and does that allocation affect innovative capacity? To answer this question, the authors build a model that develops intuitions about the strategic incentives that incumbent firms face, and how they might use the innovation input market to limit competition. The model allows for an incumbent to hire an inventor who otherwise would create an innovation inside an entrant firm and displace the incumbent. Further, since the incumbent monopolist already has a successful product, it has less incentive to innovate.

So why would an established firm with successful products spend limited resources on hiring expensive inventors? The short answer: to stifle innovation. The authors’ model implies that inventors hired by incumbent firms will, indeed, earn more by working for an incumbent, but they will also produce fewer innovations. In other words, creative destruction, the process by which new innovations replace old ones, is diminished, slowing the growth of long-run output.

The authors then take their model to the data, examining the employment history of over 760,000 US inventors, finding the following:

- Inventors are increasingly concentrated in large incumbents, less likely to work for young firms, and less likely to become entrepreneurs.

- Inventors working for incumbent firms earn more and produce less impactful innovations than inventors at young firms.

- Finally, when an inventor is hired by an incumbent, compared to a young firm, their earnings increase by 12.6 percent and their innovative output declines by 6 to 11 percent; also, these patterns are robust to alternative explanations, and are not driven by promotion to managerial positions in large incumbents, for instance. (See Figure 2.)

Bottom Line: Innovation matters, and talent is key to invention; however, this research also reveals the importance of where innovation occurs. For policymakers, the lessons are salient. First, aggregate inputs (e.g., R&D spending or inventors per capita) may give a misleading picture of innovation capacity; second, factor reallocation toward large incumbents may lower growth capacity; and third, policies that encourage more incumbent innovation might occur at the expense of entrant innovations, which are higher quality on average.

This research also points to a number of interesting, policy-relevant questions. First, what role do non-compete agreements play in explaining when inventors work for incumbents or young firms? Policies that encourage or discourage spin-offs and inventor entrepreneurship may have significant impacts on innovation and growth. Second, what role do financial frictions play in the inventor’s choice to work for incumbent firms? The availability (or lack thereof) of capital may weaken incentives for inventors to start a new firm. These and other questions will benefit from further research, and the authors’ current and recent work—with its insights into the “black box” of inventor employment—offers a valuable starting point.

1 Any opinions and conclusions expressed herein are those of the authors and do not represent the views of the U.S. Census Bureau. The Census Bureau has reviewed this data product for unauthorized disclosure of confidential information and has approved the disclosure avoidance practices applied to this release. DRB Approval Number(s): CBDRB-FY20-CES007-004, CBDRB-FY21-CES007-004, CBDRB-FY22-CES008-008, CBRDB-FY23-CES020-001, CBRDB-FY23-CES020-002. DMS Project Number 7083300.

2 TFP attempts to measure the impact of technological improvement, including worker knowledge, on economic output.

3 Akcigit, U., and N. Goldschlag (2022) “Measuring the Characteristics and Employment Dynamics of U.S. Inventors,” Discussion paper, Center for Economic Studies CES-WP-2022-43.

-

Not all inflation is created equal. While the high inflationary period of the 1970s and 1980s was marked by stock market lows not seen since the Great Depression, recent upticks in inflation have been met by rising stock values. How stocks comove with Treasury bonds has shifted over time as well. These inconsistencies present a challenge to investors seeking to safeguard their portfolios against risk, as well as for policymakers aiming to understand how financial markets respond to shocks. Motivated by this, this paper offers a framework for understanding the implications of inflation.

The authors distinguish between inflation that is “good” and that which is “bad,” using prior research to show how the two have different sources and implications for markets. They establish the following concerning “good” vs. “bad” inflation:

This framework can help policymakers and investors draw more accurate conclusions about the sources and consequences of future bouts of inflation. While it is still too early to predict the impacts of the post-COVID pandemic surge, evidence from surveys and inflation swap markets suggest that inflation risk premia are narrow. The authors conclude by offering two interpretations of these early indicators: that of the optimist, who may be relieved that inflation risk remains small, and that of the pessimist, who may worry that markets outpace beliefs, often slow to update.

-

A growing body of evidence shows that sentiment and economic growth tend to rise and fall together. However, the channel of this correlation and potential causality are unresolved. Is sentiment related to fundamentals? Is sentiment a signal of future productivity but does not cause it? Does sentiment exert an immediate and lasting effect on economic growth through a self-fulfilling feedback loop? Given the many factors that impact economic activity, isolating the effects of consumer sentiment poses a challenge.

The authors propose a novel way to address these questions by analyzing data across sixteen countries with varying degrees of efficiency in their capital markets over the period 1975 to 2019. They hypothesize that countries with less efficient capital markets respond more strongly to sentiment shocks because investors are unable to distinguish between a change in fundamentals and a change in sentiment unsupported by fundamentals, a prediction that they exploit in their research design. The authors apply four different measures of efficiency of capital markets: inclusion in the G7 group, inclusion in the Eurozone, stock turnover over GDP, and per capita GDP. The authors study how economies of varying efficiency of capital markets respond to changing sentiment, and find the following:

- In countries with efficient capital markets, positive sentiment shocks increase economic activity only temporarily and without affecting total factor productivity. Sentiment shocks predict modest increases in consumption, employment, and income for two years.

- In countries with less efficient capital markets, sentiment shocks predict more prolonged economic growth and a corresponding increase in total factor productivity. Sentiment shocks predict large increases in consumption, employment, and income for four years.

- These effects are driven largely by financial markets: with positive sentiment driving up stock prices, investors are quick to take advantage of the lowered cost of capital. The authors observe increased capital investment and their associated rate of return following sentiment shocks.

- Countries with efficient capital markets exhibit a faster mispricing correction, lending support to the authors’ hypothesis that such markets are more efficient. As a result, sentiment is a negative predictor of returns.

- By contrast, countries with less efficient capital markets exhibit a slower mispricing correction because investors misinterpret consumer optimism as a signal about better investment opportunities. As a result, sentiment is a positive predictor of returns.

This paper offers new evidence on how sentiment impacts the economy. At least in countries with less efficient capital markets, sentiment appears to be a driver of economic booms. By contrast, sentiment shocks in countries with efficient capital markets leads to only short-term fluctuations that are unrelated to productivity. More broadly, this paper demonstrates how the financial sector influences economic growth.

-

That people experiencing homelessness have worse health outcomes than those who are housed is understood. However, the extent of this disparity, especially as it pertains to mortality, has not been examined nationally or with representative data. This paper addresses that gap by providing the first national calculation of mortality for people experiencing homelessness in the United States. In doing so, the authors provide novel insights into the health risks associated with homelessness.

To examine this phenomenon, the authors follow for 12 years 140,000 sheltered or unsheltered homeless people counted in the 2010 Census, by far the largest and closest to representative sample of this population ever analyzed. They compare homeless individuals’ mortality vs. the housed US population overall and for sub-groups defined by age, gender, race, Hispanic ethnicity, disability status, and income (in the latter case, to examine homelessness as a risk factor for mortality that is distinct from poverty in general). The authors further examine mortality differences within the homeless population by type of homelessness, geography, demographic characteristics, income, employment status, and the extent of observed family connections. Their findings include the following:

- Non-elderly people who have experienced homelessness face 3.5 times higher mortality risk than people who are housed, accounting for differences in demographic characteristics and geography.

- This disparity far exceeds the mortality gap between Black and white housed individuals (1.4), and between poor housed and all housed individuals (2.2).

- Importantly, homelessness is associated with 60 percent greater mortality risk than poverty alone.

- Homeless individuals’ mortality risk is four times higher in their 30s and 40s. Beginning in their 50s, homeless individuals’ mortality hazard begins to converge with people who are housed, which may reflect both excess mortality of exceptionally vulnerable homeless individuals at younger ages, and shared health vulnerabilities for elderly homeless and housed individuals.

- Black homeless individuals have about 27 percent lower mortality risk than white homeless individuals, perhaps related to the lower prevalence of substance abuse and behavioral health issues among Black homeless individuals, among other factors.

- Homeless individuals without formal employment, those with lower incomes, and those without observed family connections are especially vulnerable.

- Increased mortality risks also hold for sheltered homeless individuals, which illustrates the substantial health risks faced by people experiencing homelessness even when they are not sleeping on the streets.

- Finally, regarding COVID-19: Homeless individuals’ mortality rose by 33 percent during the pandemic. While the proportional rise in mortality risk was similar for people who were housed (29.8 percent) and poor and housed (33.9 percent), the pandemic affected a much larger share of the homeless population because of their substantially elevated baseline mortality risk.

Bottom line: This work shines a bright light on health issues related to homelessness, which has drawn renewed interest recently in light of the epidemic of deaths from opioids and the impact of COVID-19 on the homeless community. The authors’ findings are broadly summarized in one startling illustration: A 40-year-old homeless person has a mortality risk similar to a housed person who is nearly 60, and a poor housed person who is nearly 50. This fact, among the many others revealed in this work, not only adds to the emerging picture of the persistent hardships and stark health disparities associated with homelessness, but also informs future analysis of safety net and other programs meant to aid the homeless.

-

Researchers have long looked to parental income as a key factor in determining intergenerational mobility. However, parental income is not fixed over time, and parental expenditures on children change as a child ages, from predominantly food, health, and shelter when a child is young, for example, to education and neighborhoods through adolescence. As this new research reveals, taking a trajectories-based approach to income and expenditures delivers important new insights into intergenerational mobility.

The authors’ trajectories-based approach allows them to link parental income at each offspring age to the child’s future permanent income. Among other features of the authors’ methodology, their approach offers more precision when measuring age-specific parental income effects (please see the working paper for more details). The authors find the following:

- There is clear evidence that a child’s permanent income is sensitive to the timing of parental income: parental incomes in middle and late adolescence are associated with larger marginal effects on predicted offspring income than earlier parental income years. This is owing, at least in part, to the increasing role of education and social influences.

- The mobility process has changed across cohorts defined as births in 1967-1970, 1971-1973, and 1974-1977: the effects of a permanent parental income starting at birth are larger for the earliest cohort compared to the two later ones. In other words, the sensitivity of offspring to income in later childhood and adolescence seems to have declined relative to the first cohort.

- The authors uncover interactions between incomes at different ages as a distinct determinant of a child’s permanent income on parental income trajectories. In doing so, they find evidence of interactions between parental incomes at different ages in terms of their effects on children.

- Finally, in an important confirmation of their income results, the authors find that family income trajectories exhibit similar influences on education as they do for income; however, their results for occupations are mixed and imprecise.

Bottom line: Parental income plays different roles over the life of a child and, likewise, has different effects at given ages. This work reveals how the measurement of intergenerational mobility is enhanced by a consideration of how the dynamics of family income over childhood and adolescence predict adult outcomes. Importantly, for those interested in the role of parental income in intergenerational mobility, this work suggests an especially important role for incomes in adolescence.

-

Human capital was first popularized by Gary Becker, who compared individuals’ investments in education and training to those of businesses in machinery and equipment. Today, scholars studying human capital often aim to identify ways to bolster peoples’ life trajectories, such as through improvements in education or health. In this paper, the authors use data on workplace injuries to study how workers invest in human capital after losing ability, and to assess the effectiveness of human capital programs that aid those workers.

They begin by linking Danish injury claims data to information on workers’ health, education, receipt of government transfers, and employment. The authors restrict their sample to the subset of people who worked steadily until an accident limited their earnings. Their data reveal the following patterns:

- Most workers do not invest in human capital following an accident, with only 13% enrolling in a degree program at any level in the ten years following their injury.

- Among those who do invest, four-year bachelor’s programs are most common. Injured workers tend to pursue fields that are less physically demanding and more cognitively intense than their previous positions, often targeting degrees that build on their experience. For example, many carpenters obtain bachelor’s degrees in construction architecture.

The authors next turn to measuring the impacts of these investments. By comparing the outcomes of otherwise-similar workers who differ only in their eligibility for Danish degree programs, they find the following:

- Reskilling through higher education improves injured workers’ labor market outcomes considerably. Roughly 80% of injured workers who reskill find employment within seven years of their accidents, on average earning 25% more than before their injuries.

- Higher education appears to mitigate other hardships associated with workplace injuries as well. While workers who do not reskill receive disability benefits from the government and are often prescribed antidepressants, those who reskill do not experience an uptick in either.

- These increased tax revenues and decreased social expenditures mean that reskilling subsidies for injured workers pay for themselves four times over.

Given these benefits, should policies to increase the share of injured workers who reskill through higher education be implemented? To answer this question, the authors assess whether the returns documented above hold as more workers reskill. They find that the share of injured workers who reskill through higher education could be expanded considerably, from 11% to 33%, to maximize returns to workers and taxpayers. The case is even stronger for middle-aged workers, who tend to reskill at lower rates despite the benefits.

The upshot is that higher education is effective at helping manual workers reskill and shift occupations. Policies that expand access to higher education could help alleviate displacement shocks to manual occupations, such as automation or globalization.

-

Women experience on average worse economic outcomes than men, from lack of basic freedom to work outside the home in some contexts to persistent underrepresentation in public and private leadership positions around the world. It is now well understood that gender norms shape some of these outcomes. More recently, economists have begun to recognize that perceived gender norms may play an important role, too: people may make incorrect assumptions about the support for gender equality or the degree to which it already exists, and such assumptions can restrict progress.

For example, recent work by one of two of the authors of this new research, UChicago economist Leonardo Bursztyn and David Yanagizawa-Drott from Zurich (together with UChicago’s Alessandra González) reveals that the vast majority of men in Saudi Arabia privately support women working outside the home, but underestimate the extent to which others share this view (see BFI Research Brief and Working Paper “Misperceived Social Norms: Women Working Outside the Home in Saudi Arabia”1). The authors show that a simple policy intervention corrects such misperceptions and leads to a significant increase in women’s involvement in labor markets. If men are informed, for example, that other men share their views, then such ideas become more publicly acceptable and, thus, advance change for women.

However, do these findings hold across space? Do they only apply to the particular cultural constructs within Saudi Arabia, or do they hold for all countries, even those with more gender-equal norms? To address these and related questions, the authors of this new research employ a novel dataset from 60 countries, as a new module of the Gallup World Poll 2020, representing over 80% of the world population. The survey measures the respondents’ support for two distinct policy-relevant issues: 1) whether women should be free to work outside of their home (basic rights), and 2) whether women should be given priority women when hiring for leadership positions (affirmative action). Crucially, the survey also measures perceived norms, i.e., what each respondent thought the support for these issues people in their country is. Perceptions were elicited separately for the support among men and the support among women. This novel dataset reveals the following insights:

- There is widespread support for women’s basic right to work outside of the home across the world: a majority of the population is in favor in all 60 countries, often by a wide margin. Importantly, while the share of women in favor is essentially always higher, a majority of men favor women’s basic rights in all countries.

- In all countries in the sample, respondents on average underestimate the extent to which people in their country support women’s basic right to work outside the home, and particularly men’s support. These findings are in line with what documented in Saudi Arabia, but on a global scale.

- Regarding affirmative action, the authors find majority support from both men and women in 37 countries, while in 12 countries a majority of both do not support it. Further, affirmative action for women is strongly negatively associated with the level of gender equality in the country, with, on average, the majority of the population being against affirmative action for women in the most gender-equal countries. Similar to basic rights, more women than men support affirmative action for women in virtually all countries.

- Perceptions of others’ support for affirmative action exhibit a perhaps surprising pattern. Just as for basic rights, in less gender-equal countries, men’s support is systematically underestimated. In more gender-equal countries, women’s support is instead systematically overestimated.

- The authors also consider potential mechanisms that could be driving the documented misperceptions and find two nearly universal forces at play: the overweighting of the minority view and widespread stereotyping of men and women.

Bottom line: Around the world, people underestimate support for basic women’s rights. This work reveals that restricting female employment based on perceived peers’ opinion is likely acting erroneously. Aligning perceived and actual views, then, may raise female labor force participation outside the home by shifting perceived social norms in a way that is actually consistent with the underlying opinions of a society. The implications for affirmative action are less clean-cut, but the study suggests that in countries like the United States, women may be substantially less in favor of such policy than widely believed (for example, women may infer that affirmative action will devalue their achievements.) Finally, while heterogeneity across countries does not lend itself to broad policy prescriptions, the authors’ methodology offers interventions that could align actual and perceived norms, and thereby move countries to embrace greater gender equality.

1 Published in the American Economic Review (2020), 110(10): 2997-3029.

-

Firearm regulations are subject to fierce political debate in the United States, with common policy proposals ranging from sweeping bans to open markets. Most research on the matter has focused on crime, with researchers often assessing the extent to which historical policy changes have or have not reduced gun crimes. This paper offers a new framework for evaluating gun regulations that incorporates the preferences of the consumer.

To understand the advantages to this approach, consider a hypothetical gun buyer. How will they respond to a price hike on their preferred firearm? Will they opt for a different (possibly deadlier) model? Or will they abstain from purchasing altogether?

Accounting for consumers’ preferences can help policymakers evaluate how well different policies will achieve their intended goals and at what cost to gun owners. Motivated by this, this paper estimates a full demand system for firearms.

The authors use a special survey, called stated choice based conjoint analysis, to collect data on consumer demand for firearms. They present respondents, who are drawn from the general public, with a series of hypothetical gun purchasing scenarios in which prices and options are set experimentally. The authors apply the resulting data to a demand model, which they validate by comparing its outputs to external data including background checks and prices. Their analysis reveals the following:

- Gun buyers aren’t very responsive to price changes, but demand for handguns is most price sensitive.

- There is considerable substitution from assault weapons to handguns, but very little substitution from handguns to assault weapons.

- Those considering purchasing their first gun tend to be more sensitive to price increases and also tend to prefer handguns more than repeat buyers.

What do these substitution patterns mean for policy? The authors conclude by using their demand model to predict the impacts of three policy scenarios: an assault weapons ban, a handgun ban, and a tax that increases the price of all firearms by 10%. They find the following:

- Banning assault weapons would lead more consumers to purchase handguns, the type of weapon involved in the majority of gun deaths.

- By contrast, banning handguns would lead to fewer firearm sales overall. A handgun ban would also result in a large reduction in consumer surplus to the many buyers who prefer handguns, a tradeoff that may limit the political feasibility of the policy.

- A 10% price increase would lead to only a small reduction in sales, suggesting that while the policy might have limited scope for reducing firearm purchases, it could generate tax revenue.

- The authors also use their demand estimates to forecast the cost of a gun buyback program. They predict that it would cost roughly $6,499 per gun to incentivize the majority of gun owners to relinquish their recent purchases.

Bottom line: This paper makes the case for incorporating consumers’ preferences in the consideration of firearm regulations. The authors’ findings concerning price sensitivity and substitution patterns have immediate impacts for policy. More broadly, their framework can be used to assess the cost and benefits of candidate firearm regulations beyond those considered here.

-

Rural Americans have worse health outcomes, yet doctors are disproportionally concentrated in large cities. For many, this long-observed phenomenon indicates that doctors are not distributed appropriately across space. Many healthcare policies have sought to “correct” this distribution. However, this new research shows more at play when considering the optimal delivery of medical services. A more complete evaluation considers two economic mechanisms crucial to understanding spatial patterns of US healthcare delivery: economies of scale and trade costs.

When the authors discuss economies of scale in medical services delivery, they are referring to classic ideas in urban economics about the benefits of geographically concentrated production. If many hospitals and doctors are located near each other, they can see more patients, specialize, and gain experience that benefits patients. They can disseminate information on the latest innovations and share the cost of specialized equipment. In other words, this spatial concentration has benefits—and especially for the people who live nearby and can easily access this high-quality care.

What about those living in rural areas, far removed from large medical centers? One way to get these patients healthcare is to distribute medical service production, including doctors, to those rural areas and forgo the benefits of scale. This is natural for time-sensitive emergency care. However, what about most other types of health care, including specialty treatments, that are scheduled in advance? Do we need a hospital with specialty practitioners in every town? Or is it better for patients to travel to big cities to see more experienced, specialized providers? If patients can travel, medical care faces a proximity-concentration trade-off like other tradable industries. In other words, patients who travel for medical services produced elsewhere incur travel costs, but they also benefit from economies of scale.

The authors assess these issues by employing Medicare claims data to quantify the roles of increasing returns to scale and trade costs in medical services. They show that larger markets produce higher quality medical services. They also show that “imported” medical procedures—defined as a patient’s consumption of a service produced by a medical provider in a different region—constitute over one-fifth of US healthcare consumption. Patients in smaller markets are the largest consumers of imported healthcare. It follows that “exports” of medical services—including specialized care—are disproportionately produced in large markets. These patterns reflect economies of scale: larger regions produce higher-quality services because they serve more patients.

The authors employ a rich dataset of millions of patient-provider interactions. They quantify how production subsidies and travel subsidies affect patients’ access to care and the quality produced in each region; the working paper describes these methods in detail. Their findings include the following:

- Production is more geographically concentrated in large markets than consumption. Since trade constitutes the difference between production and consumption, trade reduces geographic inequality in medical care access. A key implication is that common measures of healthcare production (e.g., doctors per capita) will overstate inequality in the healthcare people actually receive.

- In a theoretical model, local increasing returns to market scale can generate a home-market effect, i.e., exports of medical care rise as a region grows larger, even when prices are fixed. The authors’ model predicts that larger markets will become net exporters of medical services when local increasing returns to market scale are sufficiently strong.

- This phenomenon is borne out in the data. Local increasing returns to market scale are so strong that greater demand induces a larger increase in exports than imports. This makes larger markets net exporters of medical care and means that healthcare can serve as an export base for large urban economies.

- Larger markets produce higher-quality services thanks to economies of scale. How do we know these services are higher quality? Patients are willing to travel more to get services in these regions, all else equal. In addition, patients’ willingness to travel (revealed preference) corresponds with other measures, like US News hospital rankings.1

- A region’s quality rises considerably with the regional volume of production. While there could be many mechanisms driving this, the authors find that, in large regions, doctors are more specialized, procedures are performed by more experienced doctors, and more unique services are offered.

The authors emphasize differences between the markets for rare and common procedures.

For example, compare patients with heart failure who have left ventricular assist devices (LVADs) implanted to augment cardiac function—a rare procedure—with those who have routine screening colonoscopies. Half of the patients receiving LVAD implants come from outside the surgeon’s region, but only 15 percent of routine screening colonoscopies are performed on patients outside their home region. Their analysis reveals the following about rare procedures:- Trade and market size play a larger role for rare procedures: The imported share of consumption is 22% for common procedures and 35% for rare procedures.

- The home-market effect is substantially stronger for rare procedures: a larger residential population drives a greater increase in exports for rarer services.

- The geographic scope of the market for a medical procedure depends on its national scale: doctors performing rare procedures export their services across a broader geographic scope, sometimes serving patients who reside thousands of kilometers away. Rarer procedures are disproportionately produced and exported by large markets.

Next, the authors explore the trade-off created by putting providers proximate to patients, which also fragments the production of medical services. They find that reimbursement policies vary in how they affect patients and providers. They also affect regions differently depending on their size and trade patterns. In particular:

- A nationwide increase in reimbursements generates the largest increases in local medical care quality in the smallest regions. However, these regions’ patients experience the smallest increase in the value of market access because they consume less of their care locally.

- Reimbursement increases generate the highest return when spent in the largest cities.

But this finding comes with an important caveat: the higher-quality care available in larger markets may not benefit all patients equally. The authors show that:

- Socioeconomic status predicts how patients trade off travel costs and the benefits of scale. Patients residing in lower-income neighborhoods are less likely to travel farther for better medical care. This finding reveals that all patients do not benefit equally from local increasing returns to scale.

Bottom line for policymakers: Healthcare produced in large regions is higher quality. Policies to reallocate care to smaller regions may impact patients’ access to healthcare in unexpected ways. Traditional production subsidies in small, underserved areas help healthcare producers (e.g., doctors) more than patients in those areas. Patient travel also plays a meaningful role in enabling access to higher-quality, more experienced, and specialized care. Policymakers should consider travel subsidies rather than only production subsidies to increase access to care for underserved patients.

1 health.usnews.com/health-care/best-hospitals/articles/faq-how-and-why-we-rank-and-rate-hospitals

-

For all of its empirical and theoretical rigor, science often begins with an intuition or inspiration. Long before a new idea becomes a paper that appears in an academic journal, for example, it begins as a hypothesis. These creative suppositions commence with “data” stored in a researcher’s mind, which she then “analyzes” through a purely psychological process of pattern recognition. The “aha” moments that may follow are not necessarily inspiration, but rather the output of the researcher’s brain-driven data analysis. In other words, scientific contributions often derive from a researcher’s idiosyncratic and very human thought process.

Given the importance of scientific research and its many benefits, this raises a question: Is there a better way to generate hypotheses other than a reliance on personal analytical insight? This novel paper examines this question through the lens of machine-learning algorithms and the exploding availability of human behavior data. Second-by-second price and volume data in asset markets, high-frequency cellphone data on location and usage, CCTV camera and police “bodycam” footage, news stories, children’s books,1 the entire text of corporate filings, and so on, is now machine readable. What was once solely mental data in the service of hypothesis generation is increasingly becoming actual data.

The authors posit that these changes can fundamentally change how science gets done, which they demonstrate by developing a procedure that applies machine learning algorithms on rich data sets to generate novel hypotheses. Please see the working paper for more details, but broadly described, the authors extend the human process of generating data-driven correlations to supervised machine learning. Their new approach not only yields far more correlations than a human researcher, but it has the capacity to notice correlations that a human might never discern. This is especially true in high-dimensional data applications, potentially opening the door to research that would otherwise go unexplored.

To illustrate their procedure, which is applicable across disciplines, the authors study a high-stakes issue with profound implications: How pre-trial judges decide which defendants awaiting trial are incarcerated and which are sent free. These decisions are supposedly based on predictions of a defendant’s risk, but mounting evidence from recent research suggests that judges make these decisions imperfectly. In this case, when the authors build a deep learning model of the judge—one that predicts whether the judge will detain a given defendant—a single factor has large explanatory power: the defendant’s face.

The authors find the following:

- A predictor that uses only the pixels in the defendant’s mugshot explains from one-quarter to nearly one-half of the predictable variation in detention.

- Defendants whose mugshots fall in the bottom quartile of predicted detention are 20.4 percentage points (pp) more likely to be jailed than those in the top quartile.>

- By comparison, the difference in detention rates between those arrested for violent versus non-violent crimes is 4.8 pp.

It is important to note what this work does not reveal. The authors do not claim that a mugshot predicts a defendant’s behavior; rather their analysis reveals that mugshots predict a judge’s behavior: A defendant’s appearance correlates strongly with a judge’s decision to jail or not. And what are those appearance characteristics? There are two, and the authors label the first as “well-groomed” (e.g., tidy, clean, groomed, vs. unkempt, disheveled, sloppy look), with the second as “heavy-faced” (e.g., wide facial shape, puffier face, rounder face, heavier). Importantly, these features are not just predictive of what the algorithm sees, but also of what judges actually do:

- Both well-groomed and heavy-faced defendants are more likely released.

- Detention rates of defendants in the top and bottom quartile of well-groomedness differ by 5.5 pp (24% of the base rate) while the top vs. bottom quartile difference in heavy-facedness is 7 pp (about 30% of the base rate).

- Both differences are larger than the 4.8 pp detention rate difference between those arrested for violent vs. non-violent crimes.

Again, please see the working paper for the authors’ careful consideration of the many factors involved in their analysis, including their discussion of the ways that psychological and economic research over the past century has informed our understanding of people’s reaction to faces, including on such factors as race. The point here is that the authors’ algorithm seems to have found something new, beyond what scientists have previously hypothesized, and beyond human capability.

Bottom line: Hypothesis generation matters, and developing new ideas need not remain an idiosyncratic or nebulous process. The authors’ framework reveals that combining supervised machine learning with rich human behavior data can open the scientific world to new and fruitful lines of research. The authors’ example of judicial decision-making, along with other applications that they describe, are just the beginning. Future research will help move hypothesis generation from a pre-scientific to a scientific activity.

1 See “What We Teach About Race and Gender: Representation in Images and Text of Children’s Books,” by Anjali Adukia, et al., for a BFI Research Brief and links to the paper, an interactive tool, and video presentation.

-

The post-pandemic shift to hybrid work has revolutionized working arrangements, with US survey data revealing that one-quarter of full workdays will happen at home or other remote location after the pandemic ends, five times the pre-pandemic rate (see “Why Working From Home Will Stick”). This phenomenon, in other words, is large and enduring, and also extends beyond the United States.

In this new work, the authors shed light on work-from-home (WFH) by studying information contained in the full text of over 250 million job postings in five English-speaking countries. The authors employ state-of-the-art language-processing methods to determine whether a job allows for remote work, including identification by city, employer, industry, occupation, and other attributes. Data include almost all vacancies posted online by job boards, employer websites, and vacancy aggregators from 2014 to 2022 in Australia, Canada, New Zealand, the United Kingdom, and the United States. Importantly, vacancy postings pertain to the flow of new jobs rather than the stock of existing jobs. This is key because these new jobs entail a commitment—or at least a statement of intent—that extends into the future. (See WFHmap.com for updated, and available, data.)

The authors’ findings include the following:

- Before the pandemic in 2019, jobs offering remote work were 1% or less of all job ads in Australia, Canada, and New Zealand, about 3% in the United Kingdom, and about 4% in the United States.

- From 2019 to 2022, remote-work share rose more than three-fold in the United States and five-fold or more in the other countries.

- As of January 2023, the remote-work share exceeds 10% of postings in Australia, Canada, the United Kingdom, and the United States, and it appears to be on an upward trajectory in all five countries.

- Remote-work share correlates positively with computer use, education, and earnings, with Finance, Insurance, Information, and Communications sectors having especially high remote-work shares.

- Relatedly, Chicago, London, New York, San Francisco, Toronto, and other cities that function as business service hubs have high remote-work shares, and these differences have widened since the pandemic struck.

- Finally, this work reveals that the shift to remote work is not uniform across same-industry employers, even when they are recruiting in the same occupational category. As a result, workers now have expanded opportunities to find a job with working arrangements that suit their preferences. Importantly, this non-uniformity result also suggests that remote work is not constrained by technology; rather, it is an outcome of choices about job design and organizational management. In turn, these job design and management choices are influenced by the external environment and subject to shock-induced shifts.

A concluding note on methodology: Large-scale studies like this are not possible without machine-reading technologies that accurately discern relevant information. The authors improve upon existing methods by developing a first-of-its-kind algorithm that they label WHAM, or “Work from Home Algorithmic Measure,” to classify their 250 million job postings. WHAM achieves near-human performance in classification tasks (for example, when answering the question: “Does this text explicitly offer an employee the right to remote-work one or more days a week?”). In doing so, WHAM substantially outperforms existing methods, including the language models that underlie GPT-3 and ChatGPT, and offers future research opportunities to further explore questions surrounding the emerging WFH phenomenon.

-

Large US firms often view bankruptcy as a strategic option when facing distress, for example, by utilizing a Chapter 11 filing (reorganization) vs. Chapter 7, liquidation. As such, corporate bankruptcy can be thought of as part of the social safety net, providing some insurance against negative outcomes and giving entrepreneurs and capital providers the confidence to take risks and make important investments.

However, such benefits may prove elusive for many small and medium-sized firms, which may be unaware that bankruptcy can provide protection, for example, so a firm can negotiate with creditors to remain in business. Despite efforts to make bankruptcy more accessible and less costly for small businesses, including the February 2020 passage of the Small Business Reorganization Act (SBRA), little is known regarding small firms’ knowledge about bankruptcy. Further, the popular phrase “going bankrupt” is synonymous with closing one’s business and not preserving it, and may also suggest a commonly held stigma associated with bankruptcy that could further dissuade small- and medium sized firms from exploring its benefits.

This research examines the relationship between small- and medium-sized firms and bankruptcy by posing three questions: First, do small businesses exhibit lack of information and stigma about bankruptcy? Second, if so, is it possible to reduce the lack of information and stigma, both immediately and in the long run? Third, what are the implications for firms of reducing information unawareness and stigma?

To answer these questions, the authors conduct a novel large-scale randomized controlled trial (RCT) with US small businesses. In partnership with SCORE, the leading US organization dedicated to mentoring small businesses at all stages of development, the authors surveyed about 1,500 firms in fall 2020. Please see the working paper for more methodological details, but broadly speaking, two groups of firms were given hypothetical scenarios about a struggling business owner, with one group receiving additional information about the differences between Chapter 7 and 11 bankruptcy, or additional information that addresses stigma, including information that bankruptcy protection is fundamental to US law and is part of the US Constitution. Questions to both groups reveal the following:

- Among respondents in the Control group, almost half of the firms are unaware that it is possible for a firm to continue operations after filing for bankruptcy. Only 34% are familiar with the differences between Chapter 7 and Chapter 11 bankruptcy, and only 11% are aware that the SBRA (which was passed 9 months prior to our survey and was highly publicized) made it easier for small businesses to file for bankruptcy.

- Regarding stigma, 70% of the respondents in the Control group believe that business owners who file for bankruptcy are viewed as failures. Almost two-thirds of respondents feel that friends and family will look down on a business owner who files for bankruptcy, and over half of the entrepreneurs agree that clients and employees will be less willing to work with a business owner who has filed for bankruptcy.

- The information treatment increases the share of firms recognizing the possibility of “life after death” by 25 percentage points (pp), increases the share of firms that know that Chapter 11 is the type of bankruptcy that allows firms to continue operating by 45pp, and increases the share of firms that are aware of the SBRA by 65pp. Importantly, these effects remain strong after 4 months.

- Viewing a video about stigma greatly reduces its effects, a result that holds over the short run.

- The two treatments (Information and Information+Stigma) led firms to increase their immediate willingness to consider bankruptcy, intended investment, and intended risk-taking.

- Finally, and somewhat surprisingly given the above findings, the authors do not see longer-run real outcomes from their treatments, nor do they observe any firm actually filing for bankruptcy. The authors’ explanation of this phenomenon includes the behavioral role of entrepreneurs’ overconfidence and, to a lesser extent, excessive perceived legal fees as explanations.

Bottom line: This work reveals a stark reluctance by small businesses to take advantage of the bankruptcy protection system. For policymakers, the authors’ treatments inform potential designs for policies that attempt to further increase the use of the bankruptcy system by small businesses.

-

Key among the factors that influence whether a child grows to become an inventor are innate ability and social environment, including family resources and parental education. Parental income is a good predictor, with Figure 1 showing the relationship between the probability of off-spring becoming an inventor and parental income, using recent and historical US and Finnish data.

Why compare the United States and Finland? Because the two countries illustrate an enigma: Unlike the US, Finland displays low income inequality and high social mobility. Likewise, one would expect that income would play less of a role in Finland, with its more egalitarian society and equitable educational system.

To address this Finnish puzzle, the authors examine the little-understood role of parental education on the probability of their offspring becoming inventors. Please see the working paper for details on the authors’ methodology but, broadly speaking, they merge four datasets that include individual data on 1.45 million Finns and their parents (including, for example, parents’ distances to the nearest university at age 19), and individual-level patenting data, along with other factors, to find the following:

- While parental income is positively associated with the probability of becoming an inventor, that effect is greatly diminished once parental education is controlled for. Given that parental education is unevenly distributed, this finding informs the Finnish enigma. Moreover, as shown in Figure 2, higher parental income is positively correlated with parental education.

- Parental university education has a large, positive local average treatment effect (LATE) on the probability of a child becoming an inventor. Also, while the causal impact of parental education on sons is higher than that on daughters, the impact relative to the baseline is larger for daughters.

- The average treatment effects on the treated (ATTs) are similar to LATEs, but those on the untreated are roughly one third lower. The ATTs suggest a significant impact of parental education on the offspring, e.g., the probability of a son becoming an inventor increases by a factor of four compared to the sample average.

- Finally, Finland’s education reform implemented in the late 1960s, wherein the establishment of new universities improved parents’ ability to access higher education, has reduced the causal impact of parental education and income on the probability of inventing. In so doing, Finland both stimulated aggregate innovation and made growth more inclusive by allowing more talented individuals with low-educated parents to become innovators. Put another way, access to parental education has reduced the number of “lost Einsteins and Marie Curies” in Finland.

Bottom Line: Invention spurs growth, and a country that massively and persistently invests in education up to (STEM) PhD level can significantly increase its aggregate innovation potential, while also making innovation-led growth more inclusive. This work shows that while income matters in determining whether offspring become inventors, education is a great equalizer. Evidence from Finland, a country with low income inequality, reveals that the establishment of new universities allows higher-ability parents to study in a university, which enhances both the parents’ and their children’s human capital and skill formation in a way that increases the capacity of the offspring to invent.

-

Customer bias can take a toll on workers who are evaluated on customer service. Over time, worker performance may suffer, impacting their productivity and ultimately their pay and advancement opportunities. For firms, customer bias can be a factor in hiring and promotion decisions, while for regulators it can influence their understanding of the effects of certain policies, like performance-based pay. Despite these and other known consequences of customer bias, little is known about the magnitude of these effects.

To address this gap and the challenges of measuring the impact of customer bias (including subjective data, multiple factors like skill levels and workplace environment, and testing across equally productive individuals), the authors run the first randomized field experiment on customer discrimination for workers within a firm. They partner with an online travel agency with offices across Sub-Saharan Africa that sells flights and hotels, and that hires local sales agents to assist customers. The authors study over 2,000 customers from 70 countries (87% from Africa, 13% abroad) as they chat with online sales agents who answer their questions and help them make purchases. This allows the researchers to precisely measure worker productivity through sales records and document rich patterns of customer engagement, including bargaining and harassment, through chat transcripts.

Please see the working paper for more details on methodology, but broadly speaking the authors apply a novel framework for estimating the causal effect of customer-based discrimination, which includes randomization of the worker names and implied genders that customers see, while blocking this information from the workers themselves. Consequently, any change in consumer behavior toward sales agents could only occur if consumers respond to the randomly assigned names. This work improves upon the limitations of existing research that includes actors and fictitious scenarios to uncover bias, to find the following striking results:

- Randomly assigned female names reduce the likelihood that customers make any purchase, the number of purchases customers will make, and the value of those purchases.