Insights / Research Brief•Jun 12, 2024

Discount Factors and Monetary Policy: Evidence from Dual-Listed Stocks

Quentin Vandeweyer, Minghao Yang, Constantine Yannelis

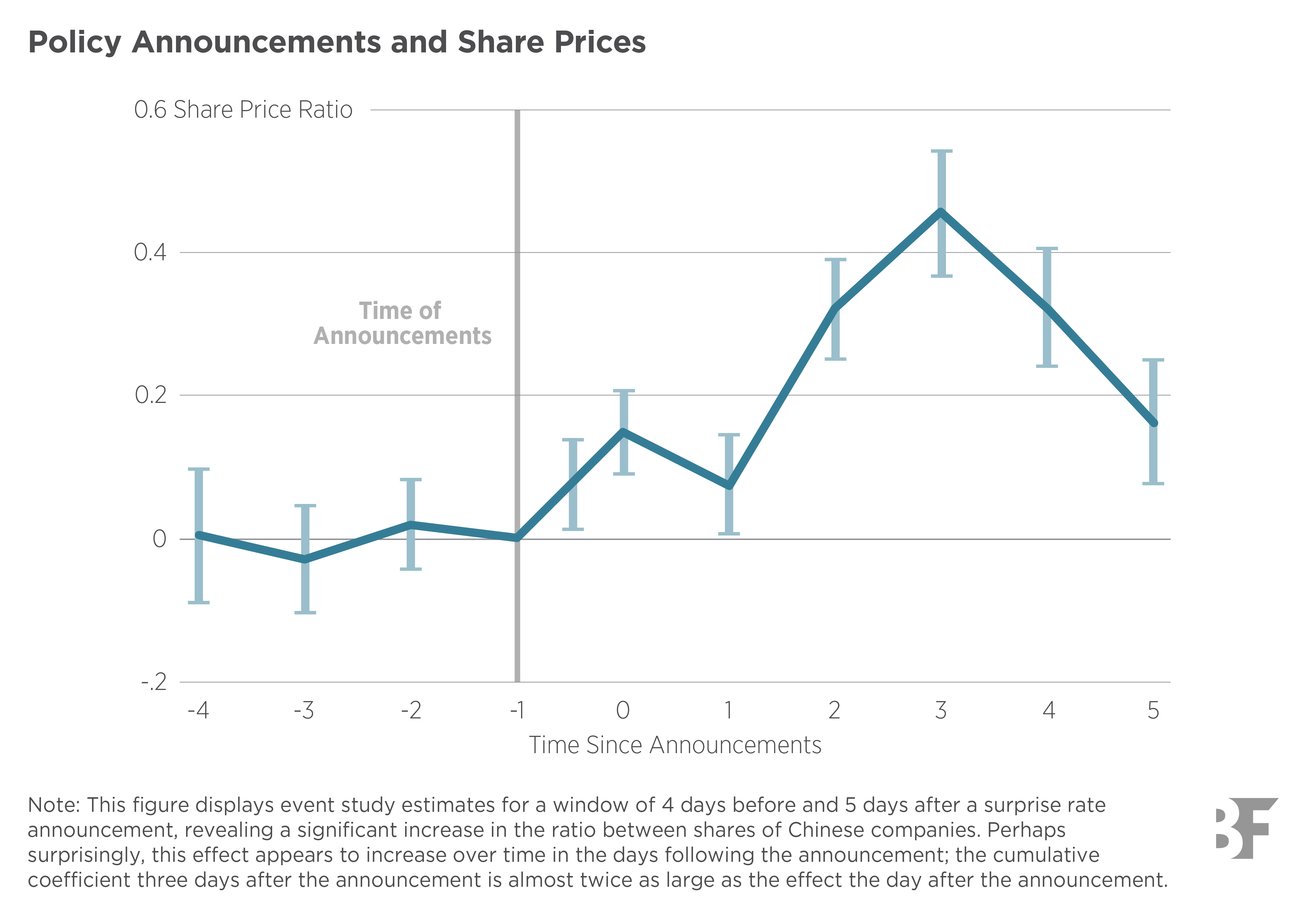

Surprise changes in US monetary policy rates directly affect asset prices, with a 100-basis point surprise cut resulting in a 30-basis point increase in the ratio of stock prices over 5 days; this effect grows after the initial announcement because higher-frequency strategies likely underestimate the effects of policy transmission.

Based on BFI Working Paper 2024-64, “Discount Factors and Monetary Policy: Evidence from Dual-Listed Stocks”